Narzędzia użytkownika

Narzędzia witryny

Pasek boczny

en:statpqpl:wielowympl

Spis treści

Multidimensional models

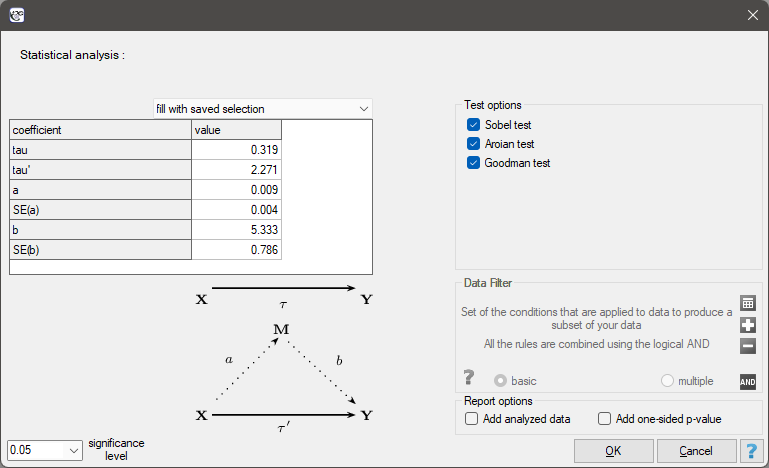

Multivariate regression models provide an opportunity to study the effects of multiple independent variables (multiple factors) and their interactions on a single dependent variable. Through multivariate models, it is also possible to build many simplified models at the same time - one-dimensional (univariate) models. The information about which model we want to build (multivariate or univariate) is visible in the window of the selected analysis. When multiple independent variables are simultaneously selected in the analysis window, it is possible to choose the model.

Preparation of variables for analysis

Matching groups

Why is group matching done?

There are many answers to this question. Let us use an example of a medical situation.

If we estimate the treatment effect from a fully randomized experiment, then by randomly assigning subjects to the treated and untreated groups we create groups that are similar in terms of possible confounding factors. The similarity of the groups is due to the random assignment itself. In such studies, we can examine the pure (not dependent on confounding factors) effect of the treatment method on the outcome of the experiment. In this case, other than random group matching is not necessary.

The possibility of error arises when the difference in treatment outcome between treated and untreated groups may be due not to the treatment itself, but to a factor that induced people to take part in the treatment. This occurs when randomization is not possible for some reason, such as it is an observational study or for ethical reasons we cannot assign treatment arbitrarily. Artificial group matching may then be applicable. For example, if the people we assign to the treatment group are healthier people and the people who are in the control group are people with more severe disease, then it is not the treatment itself but the condition of the patient before treatment that may affect the outcome of the experiment. When we see such an imbalance of groups, it is good if we can decide to randomize, in this way the probem is solved, because drawing people into groups makes them similar. However, we can imagine another situation. This time the group we are interested in will not be treatment subjects but smokers, and the control group will be non-smokers, and the analyses will aim to show the adverse effect of smoking on the occurrence of lung cancer. Then, in order to test whether smoking does indeed increase the risk of lung cancer, it would be unethical to perform a fully randomized trial because it would mean that people randomly selected to the risk group would be forced to smoke. The solution to this situation is to establish an exposure group, i.e. to select a number of people who already smoke and then to select a control group of non-smokers. The control group should be selected because by leaving the selection to chance we may get a non-smoking group that is younger than the smokers only due to the fact that smoking is becoming less fashionable in our country, so automatically there are many young people among the non-smokers.The control should be drawn from non-smokers, but so that it is as similar as possible to the treatment group.In this way we are getting closer to examining the pure (independent of selected confounding factors such as age) effect of smoking/non-smoking on the outcome of the experiment, which in this case is the occurrence of lung cancer. Such a selection can be made by the matching proposed in the program.

One of the main advantages of investigator-controlled matching is that the control group becomes more similar to the treatment group, but this is also the biggest disadvantage of this method. It is an advantage because our study is looking more and more like a randomized study. In a randomized trial, the treatment and control groups are similar on almost all characteristics, including those we don't study - the random allocation provides us with this similarity. With investigator-controlled matching, the treatment and control groups become similar on only selected characteristics.

Ways of assessing similarity:

The first two methods mentioned are based on matching groups through Propensity Score Matching, PSM. This type of matching was proposed by Rosenbaum and Rubin 1). In practice, it is a technique for matching a control group (untreated or minimally/standardly treated subjects) to a treatment group on the basis of a probability describing the subjects' propensity to assign treatment depending on the observed associated variables. The probability score describing propensity, called the Propensity Score is a balancing score, so that as a result of matching the control group to the treatment group, the distribution of measured associated variables becomes more similar between treated and untreated subjects. The third method does not determine the probability for each individual, but determines a distance/dissimilarity matrix that indicates the objects that are closest/most similar in terms of multiple selected characteristics.

Methods for determining similarity:

- Known probability – the Propensity Score, which is a value between 0 and 1 for each person tested, indicates the probability of being in the treatment group. This probability can be determined beforehand by various methods. For example, in a logistic regression model, through neural networks, or many other methods. If a person in the group from which we draw controls obtains a Propensity Score similar to that obtained by a person in the treatment group, then that person can enter the analysis because the two are similar in terms of the characteristics that were considered in determining the Propensity Score.

- Calculated from the logistic regression model – because logistic regression is the most commonly used matching method, PQStat provides the ability to determine a Propensity Score value based on this method automatically in the analysis window. The matching proceeds further using the Propensity Score thus obtained.

- Similarity/distance matrix – This option does not determine the value of Propensity Score, but builds a matrix indicating the distance of each person in the treatment group to the person in the control group. The user can set the boundary conditions, e.g. he can indicate that the person matched to a person from the treatment group cannot differ from him by more than 3 years of age and must be of the same sex. Distances in the constructed matrix are determined based on any metric or method describing dissimilarity. This method of matching the control group to the treated group is very flexible. In addition to the arbitrary choice of how the distances/dissimilarity are determined, in many metrics it allows for the indication of weights that determine how important each variable is to the researcher, i.e., the similarity of some variables may be more important to the researcher while the similarity of others is less important. However, great caution is advised when choosing a distance/ dissimilarity matrix. Many features and many sops to determine distances require prior standardization or normalization of the data, moreover, choosing the inverse of distance or similarity (rather than dissimilarity) may result in finding the most distant and dissimilar objects, whereas we normally use these methods to find similar objects. If the researcher does not have specific reasons for changing the metric, the standard recommendation is to use statistical distance, i.e. the

Mahalanobiametric – It is the most universal, does not require prior standardization of data and is resistant to correlation of variables. More detailed description of distances and dissimilarity/similarity measures available in the program as well as the method of inetrpratation of the obtained results can be found in the Similarity matrix section .

In practice, there are many methods to indicate how close the objects being compared are, in this case treated and untreated individuals. Two are proposed in the program:

- Nearest neighbor method – is a standard way of selecting objects not only with a similar Propensity Score, but also those whose distance/dissimilarity in the matrix is the smallest.

- The nearest neighbor method, closer than… – works in the same way as the nearest neighbor method, with the difference that only objects that are close enough can be matched. The limit of this closeness is determined by giving a value describing the threshold, behind which there are already objects so dissimilar to the tested objects, that we do not want to give them a chance to join the newly built control group. In the case when analysis is based on Propensity Score or matrix defined by dissimilarity, the most dissimilar objects are those distant by 1, and the most similar are those distant by 0. Choosing this method we should give a value closer to 0, when we select more restrictively, or closer to 1, when the threshold will be placed further. When we determine distances instead of dissimilarities in the matrix, then the minimum size is also 0, but the maximum size is not predetermined.

We can match without returning already drawn objects or with returning these objects again to the group from which we draw.

- Matching without returning – when using no-return matching, once an untreated person has been selected for matching with a given treated person, that untreated person is no longer available for consideration as a potential match for subsequent treated persons. As a result, each untreated individual is included in at most one matching set.

- Matching with returning – return matching allows a given untreated individual to be included more than once in a single matched set. When return matching is used, further analyses, and in particular variance estimation, must take into account the fact that the same untreated individual may be in multiple matched sets.

In the case when it is impossible to match the untreated person to the treated one, because in the group from which we choose there are more persons matching the treated one equally well, then one of these persons chosen in a random way is combined. For a renewed analysis, a fixed seed is set by default so that the results of a repeated draw will be the same, but when the analysis is performed again the seed is changed and the result of the draw may be different.

If it is not possible to match an untreated person to a treated one, because there are no more persons to join in the group from which we are choosing, e.g. matching persons have already been joined to other treated persons or the set from which we are choosing has no similar persons, then this person remains without a pair.

Most often a 1:1 match is made,i.e., for one treated person, one untreated person is matched. However, if the original control group from which we draw is large enough and we need to draw more individuals, then we can choose to match 1:k, where k indicates the number of individuals that should be matched to each treated individual.

Matching evaluation

After matching the control group to the treatment group, the results of such matching can be returned to the worksheet, i.e. a new control group can be obtained. However, we should not assume that by applying the matching we will always obtain satisfactory results. In many situations, the group from which we draw does not have a sufficient number of such objects that are sufficiently similar to the treatment group. Therefore, the matching performed should always be evaluated. There are many methods of evaluating the matching of groups. The program uses methods based on standardized group difference and Propensity Score percentile agreement of the treatment group and the control group, more extensively described in the work of P.C Austin, among others 2)3). This approach allows comparison of the relative balance of variables measured in different units, and the result is not affected by sample size. The estimation of concordance using statistical tests was abandoned because the matched control group is usually much smaller than the original control group, so that the obtained p-values of tests comparing the test group to the smaller control group are more likely to be left with the null hypothesis, and therefore do not show significant differences due to the reduced size.

For comparison of continuous variables we determine the standardized mean difference:

where:

,

,  – is the mean value of the variable in the treatment group and the mean value of the variable in the control group,

– is the mean value of the variable in the treatment group and the mean value of the variable in the control group,

,

,  – is the variance in the treatment group and the variance in the control group.

– is the variance in the treatment group and the variance in the control group.

To compare binary variables (of two categories, usually 0 and 1) we determine the standardized frequency difference:

where:

,

,  – is the frequency of the value described as 1 in the treatment group and the frequency of the value described as 1 in the control group.

– is the frequency of the value described as 1 in the treatment group and the frequency of the value described as 1 in the control group.

Variables with multiple categories we should break down in logistic regression analysis into dummy variables with two categories and, by checking the fits of both groups, determine the standardized frequency difference for them.

Note

Although there is no universally agreed criterion for what threshold of standardized difference can be used to indicate significant imbalance, a standardized difference of less than 0.1 (in both mean and frequency estimation) can provide a clue 4). Therefore, to conclude that the groups are well matched, we should observe standardized differences close to 0, and preferably not outside the range of -0.1 to 0.1. Graphically, these results are presented in a dot plot. Negative differences indicate lower means/frequencies in the treatment group, positive in the control group.

Note

The 1:1 match obtained in the reports means the summary for the study group and the corresponding control group obtained in the first match, the 1:2 match means the summary for the study group and the corresponding control group obtained in the first + second match (i.e., not the study group and the corresponding control group obtained in the second match only), etc.

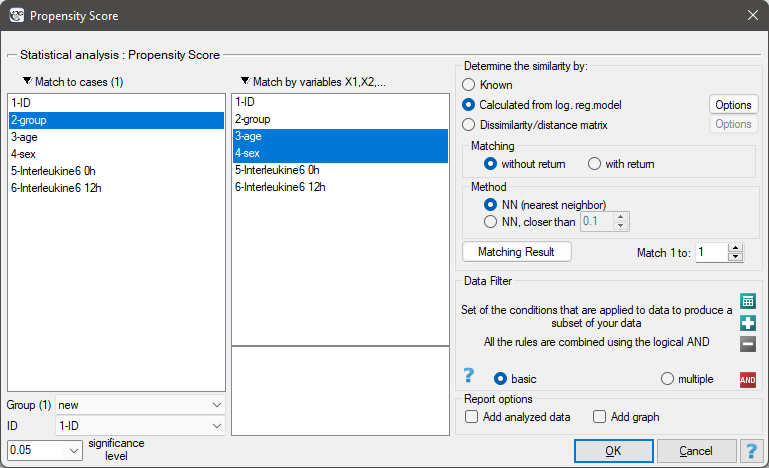

The window with the settings of group matching options is launched from the menu Advanced statistics→Multivariate models→Propensity Score

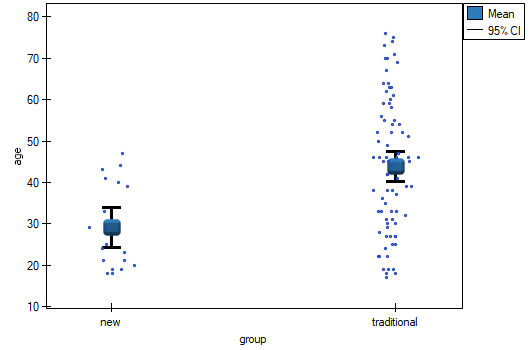

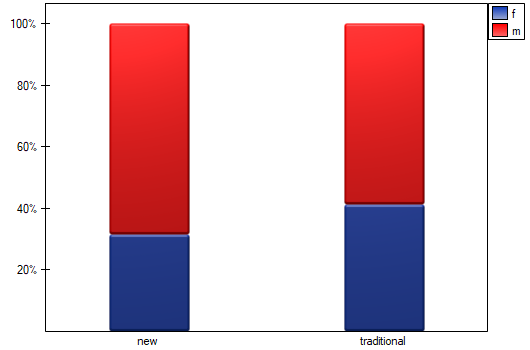

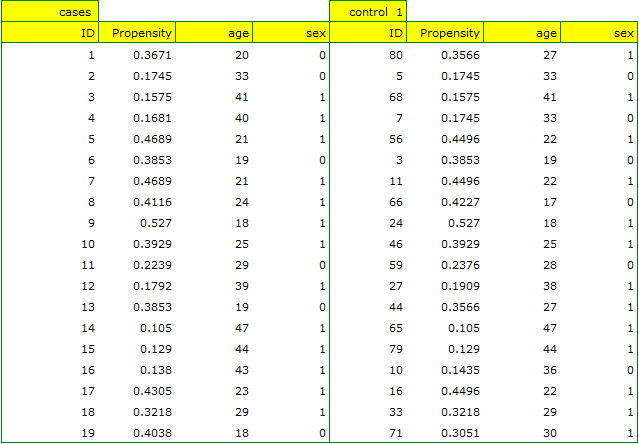

We want to compare two ways of treating patients after accidents, the traditional way and the new one. The correct effect of both treatments should be observed in the decreasing levels of selected cytokines. To compare the effectiveness of the two treatments, they should both be carried out on patients who are quite similar. Then we will be sure that any differences in the effectiveness of these treatments will be due to the treatment effect itself and not to other differences between patients assigned to different groups. The study is a posteriori, that is, it is based on data collected from patients' treatment histories. Therefore, the researchers had no influence on the assignment of patients to the new drug treatment group and the traditional treatment group. It was noted that the traditional treatment was mainly prescribed to older patients, while the new treatment was prescribed to younger patients, in whom it is easier to lower cytokine levels. The groups were fairly similar in gender structure, but not identical.

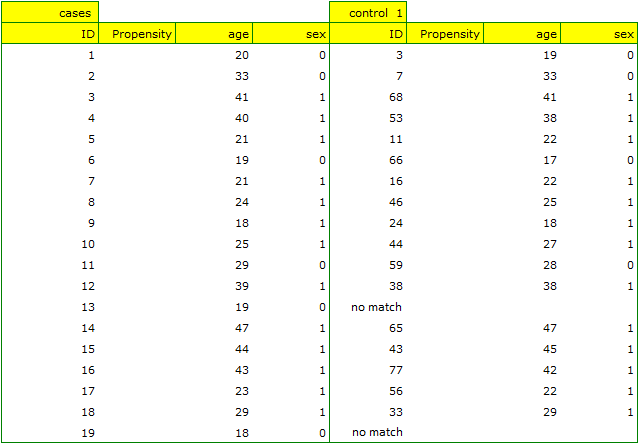

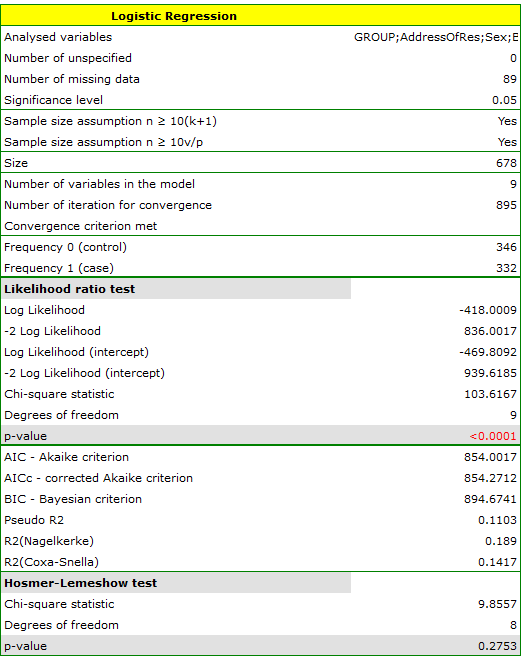

If the planned study had been carried out on such selected groups of patients, the new way would have had an easier challenge, because younger organisms might have responded better to the treatment. The conditions of the experiment would not be equal for both ways, which could falsify the results of the analyses and the conclusions drawn. Therefore, it was decided to match the group treated traditionally to be similar to the study group treated with the new way. We planned to make the matching with respect to two characteristics, i.e. age and gender. The traditional treatment group is larger (80 patients) than the new treatment group (19 patients), so there is a good chance that the groups will be similar. Random selection is performed by the logistic regression model algorithm embedded in the PSM. We remember that gender should be coded numerically, since only numerical values are involved in the logistic regression analysis. We choose nearest neighbor as the method. We want the same person to be unable to be selected duplicately, so we choose a no return randomization. We will try 1:1 matching, i.e. for each person treated with the new drug we will match one person treated traditionally. Remember that the matching is random, so it depends on the random value of seed set by our computer, so the randomization performed by the reader may differ from the values presented here.

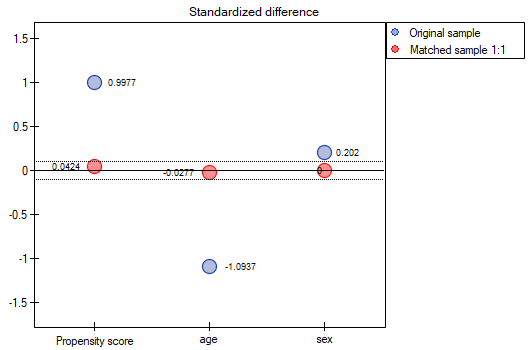

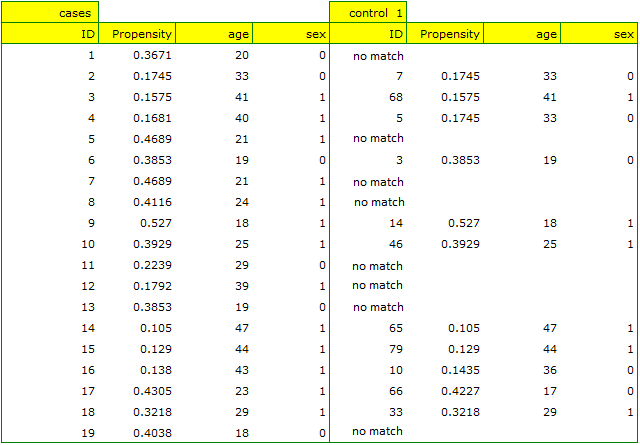

A summary of the selection can be seen in the tables and charts.

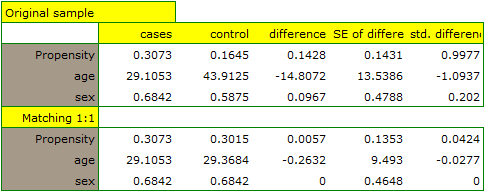

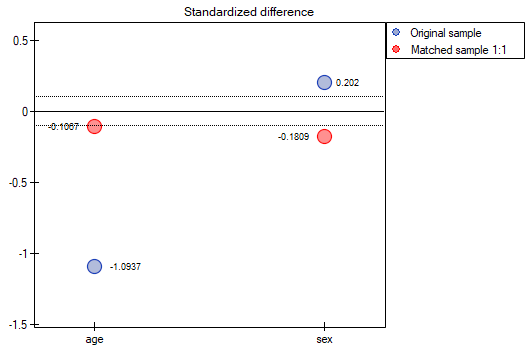

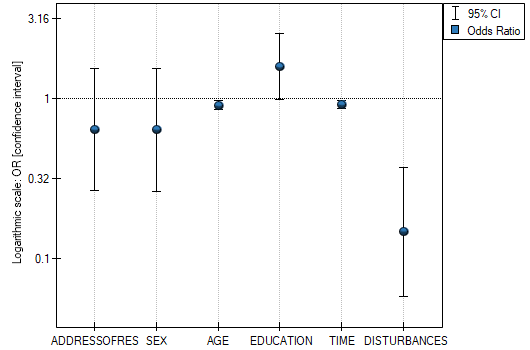

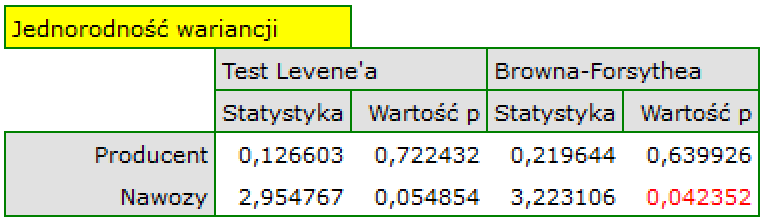

The line at 0 indicates equilibrium of the groups (difference between groups equal to 0). When the groups are in equilibrium with respect to the given characteristics, then all points on the graph are close to this line, i.e., around the interval -0.1 to 0.1. In the case of the original sample (blue color), we see a significant departure of Propensity Score. As we know, this mismatch is mainly due to age mismatch – its standardized difference is at a large distance from 0, and to a lesser extent gender mismatch.

By performing the matching we obtained groups more similar to each other (red color in the graph). The standardized difference between the groups as determined by Propensity Score is 0.0424, which is within the specified range. The age of both groups is already similar – the traditional treatment group differs from the new treatment group by less than a year on average (the difference between the averages presented in the table is 0.2632) and the standardized difference between the averages is -0.0277. In the case of gender, the match is perfect, i.e. the percentage of females and males is the same in both groups (the standardized difference between the percentages presented in the table and the graph is now 0). We can return the data prepared in this way to the worksheet and subject it to the analyses we have planned.

Looking at the summary we just obtained, we can see that despite the good balancing of the groups and the perfect match of many individuals, there are individuals who are not as similar as we might expect.

Sometimes in addition to obtaining well-balanced groups, researchers are interested in determining the exact way of selecting individuals, i.e. obtaining a greater influence on the similarity of objects as to the value of Propensity Score or on the similarity of objects as to the value of specific characteristics. Then, if the group from which we draw is sufficiently large, the analysis may yield results that are more favorable from the researcher's point of view, but if in the group from which we draw there is a lack of objects meeting our criteria, then for some people we will not be able to find a match that meets our conditions.

- Suppose that we would like to obtain such groups whose Propensity Score (i.e., propensity to take the survey) differs by no more than …

How to determine this value? You can take a look at the report from the earlier analysis, where the smallest and largest distance between the drawn objects is given.

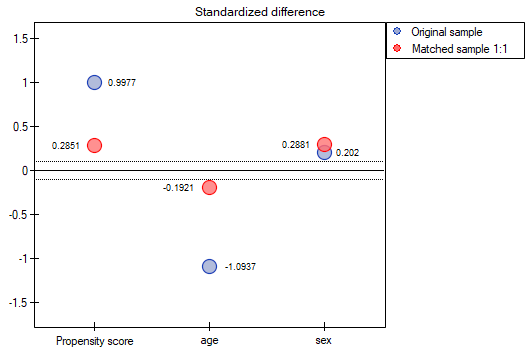

In our case the objects closest to each other differ by min=0, and the furthest by max=0.5183. We will try to check what kind of selection we will obtain when we will match to people treated with the new method such people treated traditionally, whose Propensity Score will be very close to e.g. less than 0.01.

We can see that this time with failed to select the whole group. Comparing Propensity Score for each pair (treated with the new method and treated traditionally) we can see that the differences are really small. However, since the matched group is much smaller, to sum up the whole process we have to notice that both Propensity Score, age and sex are not close enough to the line at 0. Our will to improve the situation did not lead to the desired effect, and the obtained groups are not well balanced.

- Suppose we wanted to obtain such pairs (subjects treated with the new method and subjects treated traditionally) who are of the same sex and whose ages do not differ by more than 3 years. In the Propensity Score-based randomization, we did not have this type of ability to influence the extent of concordance of each variable. For this we will use a different method, not based on Propensity Score, but based on distance/dissimilarity matrices. After selecting the

Optionsbutton, we select the proposed Mahalanobis statistical distance matrix and set the neighborhood fit to a maximum distance equal to 3 for age and equal to 0 for gender. As a result, for two people we failed to find a match, but the remaining matches meet the set criteria.

To summarize the overall draw, we note that although it meets our assumptions, the resulting groups are not as well balanced as they were in our first draw based on Propensity Score. The points in red representing the quality of the match by age and the quality of the match by gender deviate slightly from the line of sameness set at level 0, which means that the average difference in age and sex structure is now greater than in the first matching.

It is up to the researcher to decide which way of preparing the data will be more beneficial to them.

Finally, when the decision is made, the data can be returned to a new worksheet. To do this, go back to the report you selected and in the project tree under the right button select the Redo analysis menu. In the same analysis window, point to the Fit Result button and specify which other variables will be returned to the new worksheet.

This will result in a new data sheet with side-by-side data for people treated with the new treatment and matched people treated traditionally.

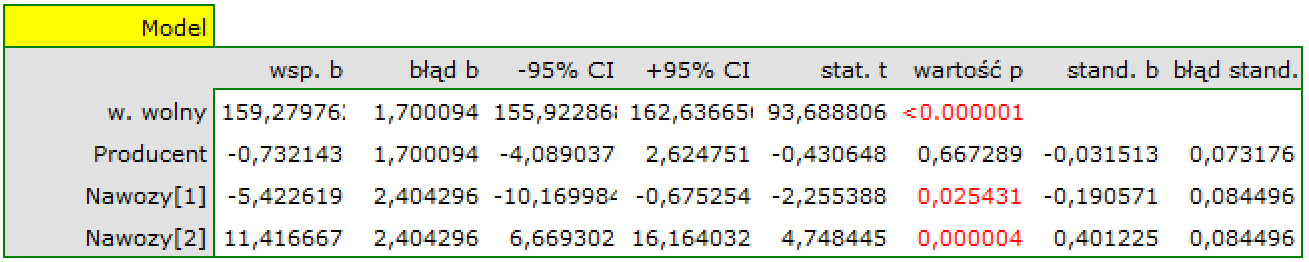

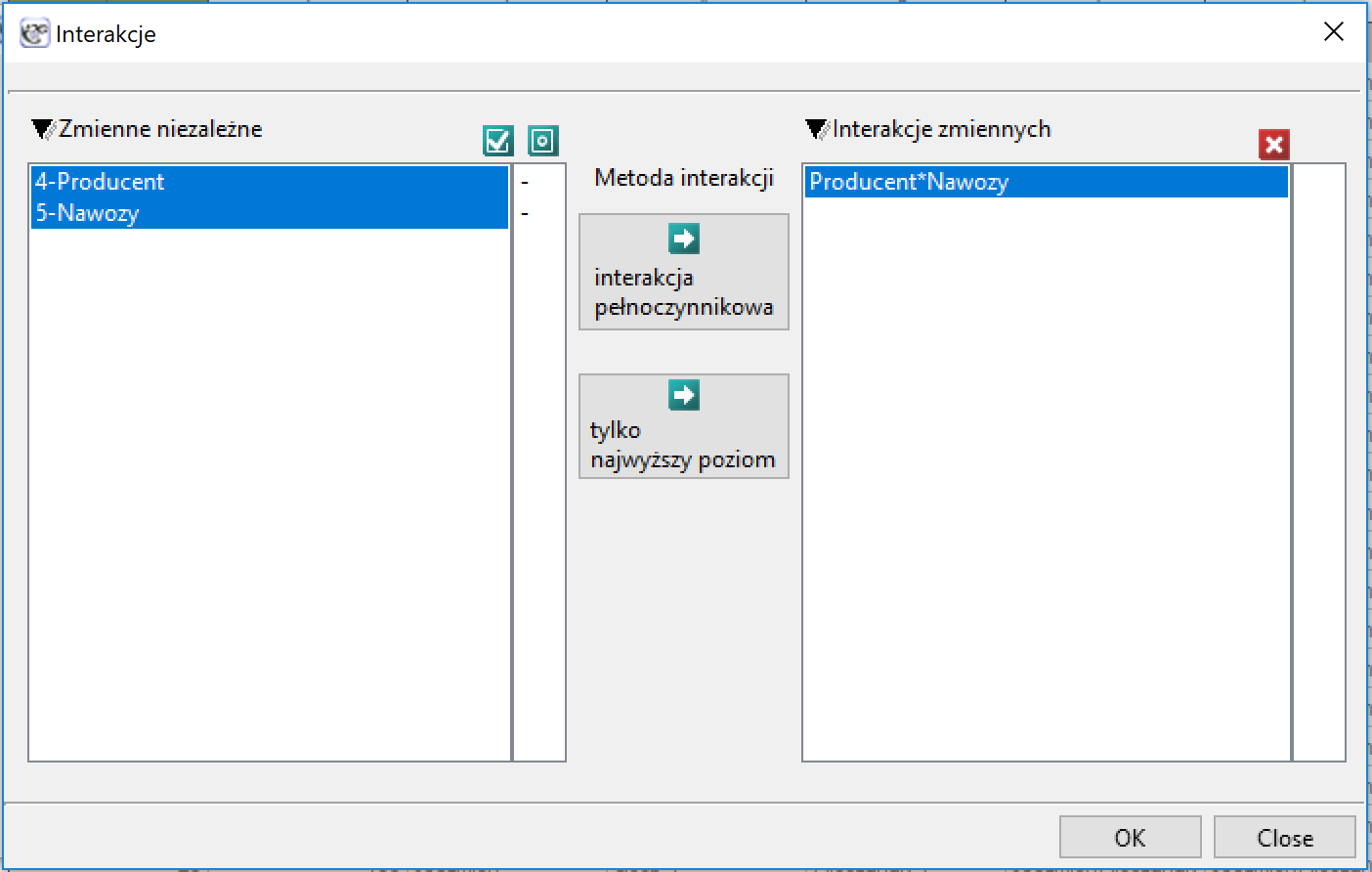

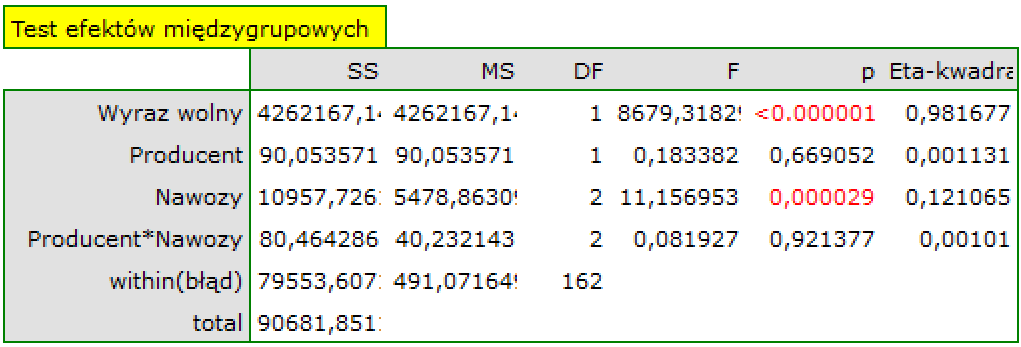

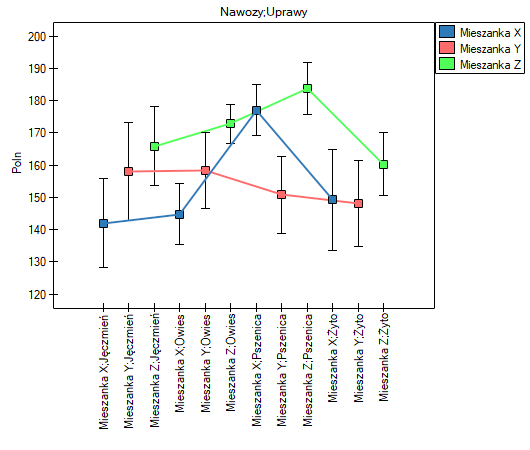

Interctions

Interactions are considered in multidimensional models. Their presence means that the influence of the independent variable ( ) on the dependent variable (

) on the dependent variable ( ) differs depending on the level of another independent variable (

) differs depending on the level of another independent variable ( ) or a series of other independent variables. To discuss the interactions in multidimensional models one must determine the variables informing about possible interactions, i.e the product of appropriate variables. For that purpose we select the

) or a series of other independent variables. To discuss the interactions in multidimensional models one must determine the variables informing about possible interactions, i.e the product of appropriate variables. For that purpose we select the Interactions button in the window of the selected multidimensional analysis. In the window of interactions settings, with the CTRL button pressed, we determine the variables which are to form interactions and transfer the variables into the neighboring list with the use of an arrow. By pressing the OK button we will obtain appropriate columns in the datasheet.

In the analysis of the interaction the choice of appropriate coding of dichotomous variables allows the avoidance of the over-parametrization related to interactions. Over-parametrization causes the effects of the lower order for dichotomous variables to be redundant with respect to the confounding interactions of the higher order. As a result, the inclusion of the interactions of the higher order in the model annuls the effect of the interactions of the lower orders, not allowing an appropriate evaluation of the latter. In order to avoid the over-parametrization in a model in which there are interactions of dichotomous variables it is recommended to choose the option effect coding.

In models with interactions, remember to „trim” them appropriately, so that when removing the main effects, we also remove the effects of higher orders that depend on them. That is: if in a model we have the following variables (main effects): , ,  and interactions:

and interactions:  ,

,  ,

,  ,

,  , then by removing the variable from the model we must also remove the interactions in which it occurs, viz: , and .

, then by removing the variable from the model we must also remove the interactions in which it occurs, viz: , and .

Variables coding

When preparing data for a multidimensional analysis there is the problem of appropriate coding of nominal and ordinal variables. That is an important element of preparing data for analysis as it is a key factor in the interpretation of the coefficients of a model. The nominal or ordinal variables divide the analyzed objects into two or more categories. The dichotomous variables (in two categories,  ) must only be appropriately coded, whereas the variables with many categories (

) must only be appropriately coded, whereas the variables with many categories ( ) ought to be divided into dummy variables with two categories and coded.

) ought to be divided into dummy variables with two categories and coded.

- [] If a variable is dichotomous, it is the decision of the researcher how the data representing the variable will be entered, so any numerical codes can be entered, e.g. 0 and 1. In the program one can change one's coding into

effect codingby selecting that option in the window of the selected multidimensional analysis. Such coding causes a replacement of the smaller value with value -1 and of the greater value with value 1. - [] If a variable has many categories then in the window of the selected multidimensional analysis we select the button

Dummy variablesand set the reference/base category for those variables which we want to break into dummy variables. The variables will be dummy coded unless theeffect codingoption will be selected in the window of the analysis – in such a case, they will be coded as -1, 0, and 1.

Dummy coding is employed in order to answer, with the use of multidimensional models, the question: How do the () results in any analyzed category differ from the results of the reference category. The coding consists in ascribing value 0 or 1 to each category of the given variable. The category coded as 0 is, then, the reference category.

- [] If the coded variable is dichotomous, then by placing it in a regression model we will obtain the coefficient calculated for it, (

). The coefficient is the reference of the value of the dependent variable for category 1 to the reference category (corrected with the remaining variables in the model).

). The coefficient is the reference of the value of the dependent variable for category 1 to the reference category (corrected with the remaining variables in the model). - [] If the analyzed variable has more than two categories, then

categories are represented by

categories are represented by  dummy variables with dummy coding. When creating variables with dummy coding one selects a category for which no dummy category is created. That category is treated as a reference category (as the value of each variable coded in the dummy coding is equal to 0.

dummy variables with dummy coding. When creating variables with dummy coding one selects a category for which no dummy category is created. That category is treated as a reference category (as the value of each variable coded in the dummy coding is equal to 0.

When the  variables obtained in that way, with dummy coding, are placed in a regression model, then their

variables obtained in that way, with dummy coding, are placed in a regression model, then their  coefficients will be calculated.

coefficients will be calculated.

- [

] is the reference of the results (for codes 1 in ) to the reference category (corrected with the remaining variables in the model);

] is the reference of the results (for codes 1 in ) to the reference category (corrected with the remaining variables in the model); - [

] is the reference of the results (for codes 1 in ) to the reference category (corrected with the remaining variables in the model);

] is the reference of the results (for codes 1 in ) to the reference category (corrected with the remaining variables in the model); - […]

- [

] is the reference of the results (for codes 1 in

] is the reference of the results (for codes 1 in  ) to the reference category (corrected with the remaining variables in the model);

) to the reference category (corrected with the remaining variables in the model);

Example

We code, in accordance with dummy coding, the sex variable with two categories (the male sex will be selected as the reference category), and the education variable with 4 categories (elementary education will be selected as the reference category).

![\mbox{\begin{tabular}{|c|c|}

\hline

&\textcolor[rgb]{0.5,0,0.5}{\textbf{Coded}}\\

\textbf{Sex}&\textcolor[rgb]{0.5,0,0.5}{\textbf{sex}}\\\hline

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}0\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}0\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}0\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}0\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}0\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}0\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}0\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}0\\

...&...\\\hline

\end{tabular}](/lib/exe/fetch.php?media=wiki:latex:/img64f9c549e24e01a1c45aee7f0c4dbb3e.png "LaTeX")

![\mbox{\begin{tabular}{|c|ccc|}

\hline

& \multicolumn{3}{c|}{\textbf{Coded education}}\\

\textbf{Education}&\textcolor[rgb]{0,0,1}{\textbf{vocational}}&\textcolor[rgb]{1,0,0}{\textbf{secondary}}&\textcolor[rgb]{0,0.58,0}{\textbf{tertiary}}\\\hline

\cellcolor[rgb]{0.88,0.88,0.88}elementary&\cellcolor[rgb]{0.88,0.88,0.88}0&\cellcolor[rgb]{0.88,0.88,0.88}0&\cellcolor[rgb]{0.88,0.88,0.88}0\\

\cellcolor[rgb]{0.88,0.88,0.88}elementary&\cellcolor[rgb]{0.88,0.88,0.88}0&\cellcolor[rgb]{0.88,0.88,0.88}0&\cellcolor[rgb]{0.88,0.88,0.88}0\\

\cellcolor[rgb]{0.88,0.88,0.88}elementary&\cellcolor[rgb]{0.88,0.88,0.88}0&\cellcolor[rgb]{0.88,0.88,0.88}0&\cellcolor[rgb]{0.88,0.88,0.88}0\\

\textcolor[rgb]{0,0,1}{vocational}&\textcolor[rgb]{0,0,1}{1}&0&0\\

\textcolor[rgb]{0,0,1}{vocational}&\textcolor[rgb]{0,0,1}{1}&0&0\\

\textcolor[rgb]{0,0,1}{vocational}&\textcolor[rgb]{0,0,1}{1}&0&0\\

\textcolor[rgb]{0,0,1}{vocational}&\textcolor[rgb]{0,0,1}{1}&0&0\\

\textcolor[rgb]{1,0,0}{secondary}&0&\textcolor[rgb]{1,0,0}{1}&0\\

\textcolor[rgb]{1,0,0}{secondary}&0&\textcolor[rgb]{1,0,0}{1}&0\\

\textcolor[rgb]{1,0,0}{secondary}&0&\textcolor[rgb]{1,0,0}{1}&0\\

\textcolor[rgb]{1,0,0}{secondary}&0&\textcolor[rgb]{1,0,0}{1}&0\\

\textcolor[rgb]{0,0.58,0}{tertiary}&0&0&\textcolor[rgb]{0,0.58,0}{1}\\

\textcolor[rgb]{0,0.58,0}{tertiary}&0&0&\textcolor[rgb]{0,0.58,0}{1}\\

\textcolor[rgb]{0,0.58,0}{tertiary}&0&0&\textcolor[rgb]{0,0.58,0}{1}\\\

\textcolor[rgb]{0,0.58,0}{tertiary}&0&0&\textcolor[rgb]{0,0.58,0}{1}\\

\textcolor[rgb]{0,0.58,0}{tertiary}&0&0&\textcolor[rgb]{0,0.58,0}{1}\\

...&...&...&...\\\hline

\end{tabular}](/lib/exe/fetch.php?media=wiki:latex:/imgbfcf0cf803285f0ed297510006e88698.png "LaTeX")

Building on the basis of dummy variables, in a multiple regression model, we might want to check what impact the variables have on a dependent variable, e.g. = the amount of earnings (in thousands of PLN). As a result of such an analysis we will obtain sample coefficients for each dummy variable:

- for sex the statistically significant coefficient  , which means that average women's wages are a half of a thousand PLN lower than men's wages, assuming that all other variables in the model remain unchanged;

, which means that average women's wages are a half of a thousand PLN lower than men's wages, assuming that all other variables in the model remain unchanged;

- for vocational education the statistically significant coefficient  , which means that the average wages of people with elementary education are 0.6 of a thousand PLN higher than those of people with elementary education, assuming that all other variables in the model remain unchanged;

, which means that the average wages of people with elementary education are 0.6 of a thousand PLN higher than those of people with elementary education, assuming that all other variables in the model remain unchanged;

- for secondary education the statistically significant coefficient  , which means that the average wages of people with secondary education are a thousand PLN higher than those of people with elementary education, assuming that all other variables in the model remain unchanged;

, which means that the average wages of people with secondary education are a thousand PLN higher than those of people with elementary education, assuming that all other variables in the model remain unchanged;

- for tertiary-level education the statistically significant coefficient  , which means that the average wages of people with tertiary-level education are 1.5 PLN higher than those of people with elementary education, assuming that all other variables in the model remain unchanged;

, which means that the average wages of people with tertiary-level education are 1.5 PLN higher than those of people with elementary education, assuming that all other variables in the model remain unchanged;

Effect coding is used to answer, with the use of multidimensional models, the question: How do () results in each analyzed category differ from the results of the (unweighted) mean obtained from the sample. The coding consists in ascribing value -1 or 1 to each category of the given variable. The category coded as -1 is then the base category

- [] If the coded variable is dichotomous, then by placing it in a regression model we will obtain the coefficient calculated for it, (). The coefficient is the reference of for category 1 to the unweighted general mean (corrected with the remaining variables in the model).

- If the analyzed variable has more than two categories, then categories are represented by dummy variables with effect coding. When creating variables with effect coding a category is selected for which no separate variable is made. The category is treated in the models as a base category (as in each variable made by effect coding it has values -1).

When the variables obtained in that way, with effect coding, are placed in a regression model, then their coefficients will be calculated.

- [] is the reference of the results (for codes 1 in ) to the unweighted general mean (corrected by the remaining variables in the model);

- [] is the reference of the results (for codes 1 in ) to the unweighted general mean (corrected by the remaining variables in the model);

- […]

- [] is the reference of the results (for codes 1 in ) to the unweighted general mean (corrected by the remaining variables in the model);

Example

With the use of effect coding we will code the sex variable with two categories (the male category will be the base category) and a variable informing about the region of residence in the analyzed country. 5 regions were selected: northern, southern, eastern, western, and central. The central region will be the base one.

![\mbox{\begin{tabular}{|c|c|}

\hline

&\textcolor[rgb]{0.5,0,0.5}{\textbf{Coded}}\\

\textbf{Sex}&\textcolor[rgb]{0.5,0,0.5}{\textbf{sex}}\\\hline

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

f&\textcolor[rgb]{0.5,0,0.5}{1}\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

\cellcolor[rgb]{0.88,0.88,0.88}m&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

...&...\\\hline

\end{tabular}](/lib/exe/fetch.php?media=wiki:latex:/img1352d8cc71ff450a436fe12d8d8f68a9.png "LaTeX")

![\mbox{\begin{tabular}{|c|cccc|}

\hline

\textbf{Regions}& \multicolumn{4}{c|}{\textbf{Coded regions}}\\

\textbf{of residence}&\textcolor[rgb]{0,0,1}{\textbf{western}}&\textcolor[rgb]{1,0,0}{\textbf{eastern}}&\textcolor[rgb]{0,0.58,0}{\textbf{northern}}&\textcolor[rgb]{0.55,0,0}{\textbf{southern}}\\\hline

\cellcolor[rgb]{0.88,0.88,0.88}central&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

\cellcolor[rgb]{0.88,0.88,0.88}central&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

\cellcolor[rgb]{0.88,0.88,0.88}central&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1&\cellcolor[rgb]{0.88,0.88,0.88}-1\\

\textcolor[rgb]{0,0,1}{western}&\textcolor[rgb]{0,0,1}{1}&0&0&0\\

\textcolor[rgb]{0,0,1}{western}&\textcolor[rgb]{0,0,1}{1}&0&0&0\\

\textcolor[rgb]{0,0,1}{western}&\textcolor[rgb]{0,0,1}{1}&0&0&0\\

\textcolor[rgb]{0,0,1}{western}&\textcolor[rgb]{0,0,1}{1}&0&0&0\\

\textcolor[rgb]{1,0,0}{eastern}&0&\textcolor[rgb]{1,0,0}{1}&0&0\\

\textcolor[rgb]{1,0,0}{eastern}&0&\textcolor[rgb]{1,0,0}{1}&0&0\\

\textcolor[rgb]{1,0,0}{eastern}&0&\textcolor[rgb]{1,0,0}{1}&0&0\\

\textcolor[rgb]{1,0,0}{eastern}&0&\textcolor[rgb]{1,0,0}{1}&0&0\\

\textcolor[rgb]{0,0.58,0}{northern}&0&0&\textcolor[rgb]{0,0.58,0}{1}&0\\

\textcolor[rgb]{0,0.58,0}{northern}&0&0&\textcolor[rgb]{0,0.58,0}{1}&0\\

\textcolor[rgb]{0.55,0,0}{southern}&0&0&0&\textcolor[rgb]{0.55,0,0}{1}\\

\textcolor[rgb]{0.55,0,0}{southern}&0&0&0&\textcolor[rgb]{0.55,0,0}{1}\\

\textcolor[rgb]{0.55,0,0}{southern}&0&0&0&\textcolor[rgb]{0.55,0,0}{1}\\

...&...&...&...&...\\\hline

\end{tabular}](/lib/exe/fetch.php?media=wiki:latex:/img280b4cd6d13af15399acda93337d241b.png "LaTeX")

Building on the basis of dummy variables, in a multiple regression model, we might want to check what impact the variables have on a dependent variable, e.g. = the amount of earnings (expressed in thousands of PLN). As a result of such an analysis we will obtain sample coefficients for each dummy variable:

- for sex the statistically significant coefficient , which means that the average women's wages are a half of a thousand PLN lower than the average wages in the country, assuming that the other variables in the model remain unchanged;

- for the western region the statistically significant coefficient , which means that the average wages of people living in the western region of the country are 0.6 thousand PLN higher than the average wages in the country, assuming that the other variables in the model remain unchanged;

- for the eastern region the statistically significant coefficient  , which means that the average wages of people living in the eastern region of the country are a thousand PLN lower than the average wages in the country, assuming that the other variables in the model remain unchanged;

, which means that the average wages of people living in the eastern region of the country are a thousand PLN lower than the average wages in the country, assuming that the other variables in the model remain unchanged;

- for the northern region the statistically significant coefficient  , which means that the average wages of people living in the western region of the country are 0.4 thousand PLN higher than the average wages in the country, assuming that the other variables in the model remain unchanged;

, which means that the average wages of people living in the western region of the country are 0.4 thousand PLN higher than the average wages in the country, assuming that the other variables in the model remain unchanged;

- for the southern region the statistically significant coefficient  , which means that the average wages of people living in the southern region of the country do not differ in a statistically significant manner from the average wages in the country, assuming that the other variables in the model remain unchanged;

, which means that the average wages of people living in the southern region of the country do not differ in a statistically significant manner from the average wages in the country, assuming that the other variables in the model remain unchanged;

Multiple Linear Regression

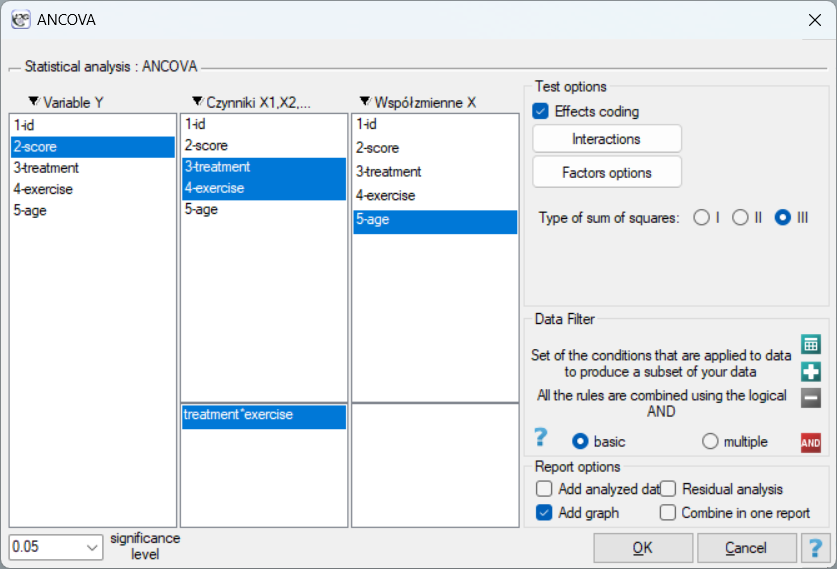

The window with settings for Multiple Regression is accessed via the menu Advanced statistics→Multidimensional Models→Multiple Regression

The constructed model of linear regression allows the study of the influence of many independent variables( ) on one dependent variable(). The most frequently used variety of multiple regression is Multiple Linear Regression. It is an extension of linear regression models based on Pearson's linear correlation coefficient. It presumes the existence of a linear relation between the studied variables. The linear model of multiple regression has the form:

) on one dependent variable(). The most frequently used variety of multiple regression is Multiple Linear Regression. It is an extension of linear regression models based on Pearson's linear correlation coefficient. It presumes the existence of a linear relation between the studied variables. The linear model of multiple regression has the form:

where:

- dependent variable, explained by the model,

- independent variables, explanatory,

- independent variables, explanatory,

- parameters,

- parameters,

- random parameter (model residual).

- random parameter (model residual).

If the model was created on the basis of a data sample of size  the above equation can be presented in the form of a matrix:

the above equation can be presented in the form of a matrix:

where:

In such a case, the solution of the equation is the vector of the estimates of parameters  called regression coefficients:

called regression coefficients:

Those coefficients are estimated with the help of the classical least squares method. On the basis of those values we can infer the magnitude of the effect of the independent variable (for which the coefficient was estimated) on the dependent variable. They inform by how many units will the dependent variable change when the independent variable is changed by 1 unit. There is a certain error of estimation for each coefficient. The magnitude of that error is estimated from the following formula:

where:

is the vector of model residuals (the difference between the actual values of the dependent variable Y and the values

is the vector of model residuals (the difference between the actual values of the dependent variable Y and the values  predicted on the basis of the model).

predicted on the basis of the model).

Dummy variables and interactions in the model

A discussion of the coding of dummy variables and interactions is presented in chapter Preparation of the variables for the analysis in multidimensional models.

Note

When constructing the model one should remember that the number of observations should meet the assumptions ( ) where is the number of explanatory variables in the model 5).

) where is the number of explanatory variables in the model 5).

Model verification

- Statistical significance of particular variables in the model.

On the basis of the coefficient and its error of estimation we can infer if the independent variable for which the coefficient was estimated has a significant effect on the dependent variable. For that purpose we use t-test.

Hypotheses:

Let us estimate the test statistics according to the formula below:

The test statistics has t-Student distribution with  degrees of freedom.

degrees of freedom.

The p-value, designated on the basis of the test statistic, is compared with the significance level  :

:

- The quality of the constructed model of multiple linear regression can be evaluated with the help of several measures.

- The standard error of estimation – it is the measure of model adequacy:

The measure is based on model residuals  , that is on the discrepancy between the actual values of the dependent variable

, that is on the discrepancy between the actual values of the dependent variable  in the sample and the values of the independent variable

in the sample and the values of the independent variable  estimated on the basis of the constructed model. It would be best if the difference were as close to zero as possible for all studied properties of the sample. Therefore, for the model to be well-fitting, the standard error of estimation (

estimated on the basis of the constructed model. It would be best if the difference were as close to zero as possible for all studied properties of the sample. Therefore, for the model to be well-fitting, the standard error of estimation ( ), expressed as

), expressed as  variance, should be the smallest possible.

variance, should be the smallest possible.

- Multiple correlation coefficient

– defines the strength of the effect of the set of variables on the dependent variable .

– defines the strength of the effect of the set of variables on the dependent variable . - Multiple determination coefficient

– it is the measure of model adequacy.

– it is the measure of model adequacy.

The value of that coefficient falls within the range of  , where 1 means excellent model adequacy, 0 – a complete lack of adequacy. The estimation is made using the following formula:

, where 1 means excellent model adequacy, 0 – a complete lack of adequacy. The estimation is made using the following formula:

where:

– total sum of squares,

– total sum of squares,

– the sum of squares explained by the model,

– the sum of squares explained by the model,

– residual sum of squares.

– residual sum of squares.

The coefficient of determination is estimated from the formula:

It expresses the percentage of the variability of the dependent variable explained by the model.

As the value of the coefficient depends on model adequacy but is also influenced by the number of variables in the model and by the sample size, there are situations in which it can be encumbered with a certain error. That is why a corrected value of that parameter is estimated:

- Information criteria are based on the entropy of information carried by the model (model uncertainty) i.e. they estimate the information lost when a given model is used to describe the phenomenon under study. Therefore, we should choose the model with the minimum value of a given information criterion.

The  ,

,  and

and  is a kind of trade-off between goodness of fit and complexity. The second element of the sum in the information criteria formulas (the so-called loss or penalty function) measures the simplicity of the model. It depends on the number of variables in the model () and the sample size (). In both cases, this element increases as the number of variables increases, and this increase is faster the smaller the number of observations.The information criterion, however, is not an absolute measure, i.e., if all the models being compared misdescribe reality in the information criterion there is no point in looking for a warning.

is a kind of trade-off between goodness of fit and complexity. The second element of the sum in the information criteria formulas (the so-called loss or penalty function) measures the simplicity of the model. It depends on the number of variables in the model () and the sample size (). In both cases, this element increases as the number of variables increases, and this increase is faster the smaller the number of observations.The information criterion, however, is not an absolute measure, i.e., if all the models being compared misdescribe reality in the information criterion there is no point in looking for a warning.

Akaike information criterion

where, the constant can be omitted because it is the same in each of the compared models.

This is an asymptotic criterion - suitable for large samples i.e. when  . For small samples, it tends to favor models with a large number of variables.

. For small samples, it tends to favor models with a large number of variables.

Example of interpretation of AIC size comparison

Suppose we determined the AIC for three models  =100,

=100,  =101.4,

=101.4,  =110. Then the relative reliability for the model can be determined. This reliability is relative because it is determined relative to another model, usually the one with the smallest AIC value. We determine it according to the formula:

=110. Then the relative reliability for the model can be determined. This reliability is relative because it is determined relative to another model, usually the one with the smallest AIC value. We determine it according to the formula:  . Comparing model 2 to model 1, we will say that the probability that it will minimize the loss of information is about half of the probability that model 1 will do so (specifically exp((100− 101.4)/2) = 0.497). Comparing model 3 to model one, we will say that the probability that it will minimize information loss is a small fraction of the probability that model 1 will do so (specifically exp((100- 110)/2) = 0.007).

. Comparing model 2 to model 1, we will say that the probability that it will minimize the loss of information is about half of the probability that model 1 will do so (specifically exp((100− 101.4)/2) = 0.497). Comparing model 3 to model one, we will say that the probability that it will minimize information loss is a small fraction of the probability that model 1 will do so (specifically exp((100- 110)/2) = 0.007).

Akaike coreccted information criterion

Correction of Akaike's criterion relates to sample size, which makes this measure recommended also for small sample sizes.

Bayes Information Criterion (or Schwarz criterion)

where, the constant can be omitted because it is the same in each of the compared models.

Like Akaike's revised criterion, the BIC takes into account the sample size.

- Error analysis for ex post forecasts:

MAE (mean absolute error) -– forecast accuracy specified by MAE informs how much on average the realised values of the dependent variable will deviate (in absolute value) from the forecasts.

MPE (mean percentage error) -– informs what average percentage of the realization of the dependent variable are forecast errors.

MAPE (mean absolute percentage error) -– informs about the average size of forecast errors expressed as a percentage of the actual values of the dependent variable. MAPE allows you to compare the accuracy of forecasts obtained from different models.

- Statistical significance of all variables in the model

The basic tool for the evaluation of the significance of all variables in the model is the analysis of variance test (the F-test). The test simultaneously verifies 3 equivalent hypotheses:

The test statistics has the form presented below:

where:

– the mean square explained by the model,

– the mean square explained by the model,

– residual mean square,

– residual mean square,

,

,  – appropriate degrees of freedom.

– appropriate degrees of freedom.

That statistics is subject to F-Snedecor distribution with  and

and  degrees of freedom.

degrees of freedom.

The p-value, designated on the basis of the test statistic, is compared with the significance level :

EXAMPLE (publisher.pqs file)

More information about the variables in the model

* Standardized  – In contrast to raw parameters (which are expressed in different units of measure, depending on the described variable, and are not directly comparable) the standardized estimates of the parameters of the model allow the comparison of the contribution of particular variables to the explanation of the variance of the dependent variable .

– In contrast to raw parameters (which are expressed in different units of measure, depending on the described variable, and are not directly comparable) the standardized estimates of the parameters of the model allow the comparison of the contribution of particular variables to the explanation of the variance of the dependent variable .

- Correlation matrix – contains information about the strength of the relation between particular variables, that is the Pearson's correlation coefficient

. The coefficient is used for the study of the corrrelation of each pair of variables, without taking into consideration the effect of the remaining variables in the model.

. The coefficient is used for the study of the corrrelation of each pair of variables, without taking into consideration the effect of the remaining variables in the model. - Covariance matrix – similarly to the correlation matrix it contains information about the linear relation among particular variables. That value is not standardized.

- Partial correlation coefficient – falls within the range

and is the measure of correlation between the specific independent variable

and is the measure of correlation between the specific independent variable  (taking into account its correlation with the remaining variables in the model) and the dependent variable (taking into account its correlation with the remaining variables in the model).

(taking into account its correlation with the remaining variables in the model) and the dependent variable (taking into account its correlation with the remaining variables in the model).

The square of that coefficient is the partial determination coefficient – it falls within the range and defines the relation of only the variance of the given independent variable with that variance of the dependent variable which was not explained by other variables in the model.

The closer the value of those coefficients to 0, the more useless the information carried by the studied variable, which means the variable is redundant.

- Semipartial correlation coefficient – falls within the range and is the measure of correlation between the specific independent variable (taking into account its correlation with the remaining variables in the model) and the dependent variable (NOT taking into account its correlation with the remaining variables in the model).

The square of that coefficient is the semipartial determination coefficient – it falls within the range and defines the relation of only the variance of the given independent variable with the complete variance of the dependent variable .

The closer the value of those coefficients to 0, the more useless the information carried by the studied variable, which means the variable is redundants.

- R-squared (

) – it represents the percentage of variance of the given independent variable , explained by the remaining independent variables. The closer to value 1 the stronger the linear relation of the studied variable with the remaining independent variables, which can mean that the variable is a redundant one.

) – it represents the percentage of variance of the given independent variable , explained by the remaining independent variables. The closer to value 1 the stronger the linear relation of the studied variable with the remaining independent variables, which can mean that the variable is a redundant one. - Variance inflation factor (

) – determines how much the variance of the estimated regression coefficient is increased due to collinearity. The closer the value is to 1, the lower the collinearity and the smaller its effect on the coefficient variance. It is assumed that strong collinearity occurs when the coefficient VIF>5 \cite{sheather}. f the variance inflation factor is 5 (

) – determines how much the variance of the estimated regression coefficient is increased due to collinearity. The closer the value is to 1, the lower the collinearity and the smaller its effect on the coefficient variance. It is assumed that strong collinearity occurs when the coefficient VIF>5 \cite{sheather}. f the variance inflation factor is 5 ( = 2.2), this means that the standard error for the coefficient of this variable is 2.2 times larger than if this variable had zero correlation with other variables .

= 2.2), this means that the standard error for the coefficient of this variable is 2.2 times larger than if this variable had zero correlation with other variables . - Tolerance =

– it represents the percentage of variance of the given independent variable , NOT explained by the remaining independent variables. The closer the value of tolerance is to 0 the stronger the linear relation of the studied variable with the remaining independent variables, which can mean that the variable is a redundant one.

– it represents the percentage of variance of the given independent variable , NOT explained by the remaining independent variables. The closer the value of tolerance is to 0 the stronger the linear relation of the studied variable with the remaining independent variables, which can mean that the variable is a redundant one. - A comparison of a full model with a model in which a given variable is removed

The comparison of the two model is made with by means of:

- F test, in a situation in which one variable or more are removed from the model (see: the comparison of models),

- t-test, when only one variable is removed from the model. It is the same test that is used for studying the significance of particular variables in the model.

In the case of removing only one variable the results of both tests are identical.

If the difference between the compared models is statistically significant (the value  ), the full model is significantly better than the reduced model. It means that the studied variable is not redundant, it has a significant effect on the given model and should not be removed from it.

), the full model is significantly better than the reduced model. It means that the studied variable is not redundant, it has a significant effect on the given model and should not be removed from it.

- Scatter plots

The charts allow a subjective evaluation of linearity of the relation among the variables and an identification of outliers. Additionally, scatter plots can be useful in an analysis of model residuals.

Analysis of model residuals

To obtain a correct regression model we should check the basic assumptions concerning model residuals.

- Outliers

The study of the model residual can be a quick source of knowledge about outlier values. Such observations can disturb the equation of the regression to a large extent because they have a great effect on the values of the coefficients in the equation. If the given residual deviates by more than 3 standard deviations from the mean value, such an observation can be classified as an outlier. A removal of an outlier can greatly enhance the model.

Cook's distance - describes the magnitude of change in regression coefficients produced by omitting a case. In the program, Cook's distances for cases that exceed the 50th percentile of the F-Snedecor distribution statistic are highlighted in bold  .

.

Mahalanobis distance - is dedicated to detecting outliers - high values indicate that a case is significantly distant from the center of the independent variables. If a case with the highest Mahalanobis value is found among the cases more than 3 deviations away, it will be marked in bold as the outlier.

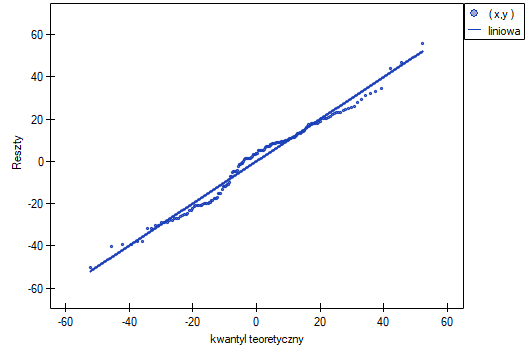

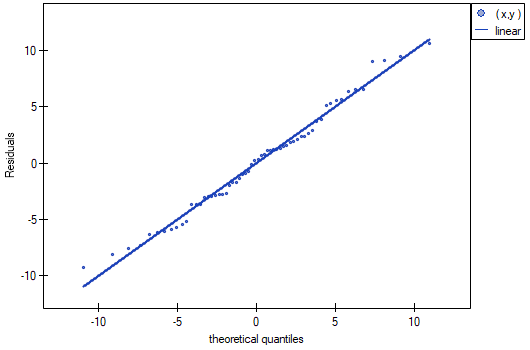

- Normalność rozkładu reszt modelu

We check this assumption visually using a Q-Q plot of the nromal distribution. The large difference between the distribution of the residuals and the normal distribution may disturb the assessment of the significance of the coefficients of the individual variables in the model.

- Homoscedasticity (homogeneity of variance)

To check if there are areas in which the variance of model residuals is increased or decreased we use the charts of:

- the residual with respect to predicted values

- the square of the residual with respect to predicted values

- the residual with respect to observed values

- the square of the residual with respect to observed values

- Autocorrelation of model residuals

For the constructed model to be deemed correct the values of residuals should not be correlated with one another (for all pairs  ). The assumption can be checked by by computing the Durbin-Watson statistic.

). The assumption can be checked by by computing the Durbin-Watson statistic.

To test for positive autocorrelation on the significance level we check the position of the statistics  with respect to the upper (

with respect to the upper ( ) and lower (

) and lower ( ) critical value:

) critical value:

- If

– the errors are positively correlated;

– the errors are positively correlated; - If

– the errors are not positively correlated;

– the errors are not positively correlated; - If

– the test result is ambiguous.

– the test result is ambiguous.

To test for negative autocorrelation on the significance level we check the position of the value  with respect to the upper () and lower () critical value:

with respect to the upper () and lower () critical value:

- If

– the errors are negatively correlated;

– the errors are negatively correlated; - If

– the errors are not negatively correlated;

– the errors are not negatively correlated; - If

– the test result is ambiguous.

– the test result is ambiguous.

The critical values of the Durbin-Watson test for the significance level  are on the website (pqstat) – the source of the: Savin and White tables (1977)6)

are on the website (pqstat) – the source of the: Savin and White tables (1977)6)

EXAMPLE cont. (publisher.pqs file)

Example for multiple regression

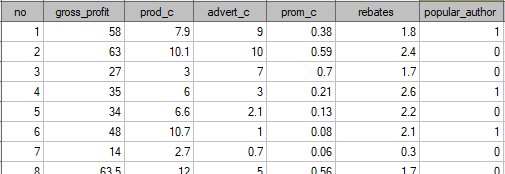

A certain book publisher wanted to learn how was gross profit from sales influenced by such variables as: production cost, advertising costs, direct promotion cost, the sum of discounts made, and the author's popularity. For that purpose he analyzed 40 titles published during the previous year (teaching set). A part of the data is presented in the image below:

The first five variables are expressed in thousands fo dollars - so they are variables gathered on an interval scale. The last variable: the author's popularity – is a dychotomic variable, where 1 stands for a known author, and 0 stands for an unknown author.

On the basis of the knowledge gained from the analysis the publisher wants to predict the gross profit from the next published book written by a known author. The expenses the publisher will bear are: production cost  , advertising costs

, advertising costs  , direct promotion costs

, direct promotion costs  , the sum of discounts made .

, the sum of discounts made .

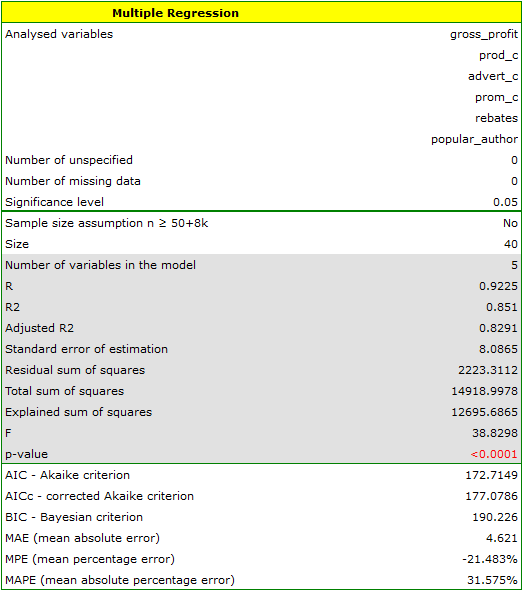

We construct the model of multiple linear regression, for teaching dataset, selecting: gross profit – as the dependent variable , production cost, advertising costs, direct promotion costs, the sum of discounts made, the author's popularity – as the independent variables  . As a result, the coefficients of the regression equation will be estimated, together with measures which will allow the evaluation of the quality of the model.

. As a result, the coefficients of the regression equation will be estimated, together with measures which will allow the evaluation of the quality of the model.

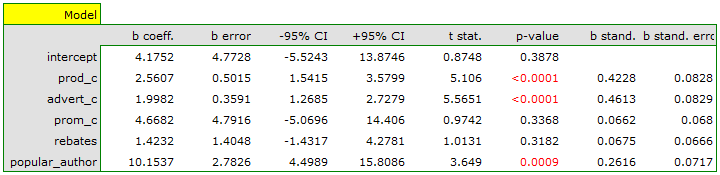

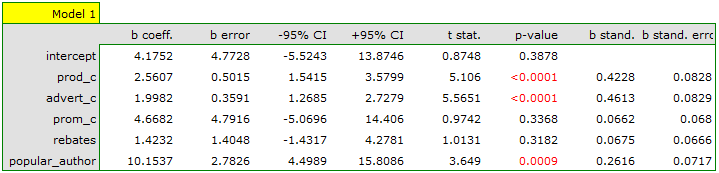

On the basis of the estimated value of the coefficient  , the relationship between gross profit and all independent variables can be described by means of the equation:

, the relationship between gross profit and all independent variables can be described by means of the equation:

![\begin{displaymath}

profit_{gross}=4.18+2.56(c_{prod})+2(c_{adv})+4.67(c_{prom})+1.42(discounts)+10.15(popul_{author})+[8.09]

\end{displaymath}](/lib/exe/fetch.php?media=wiki:latex:/imgc5f842ab62ffad495467b9baeb4f9412.png "LaTeX") The obtained coefficients are interpreted in the following manner:

The obtained coefficients are interpreted in the following manner:

- If the production cost increases by 1 thousand dollars, then gross profit will increase by about 2.56 thousand dollars, assuming that the remaining variables do not change;

- If the production cost increases by 1 thousand dollars, then gross profit will increase by about 2 thousand dollars, assuming that the remaining variables do not change;

- If the production cost increases by 1 thousand dollars, then gross profit will increase by about 4.67 thousand dollars, assuming that the remaining variables do not change;

- If the sum of the discounts made increases by 1 thousand dollars, then gross profit will increase by about 1.42 thousand dollars, assuming that the remaining variables do not change;

- If the book has been written by a known author (marked as 1), then in the model the author's popularity is assumed to be the value 1 and we get the equation:

If the book has been written by an unknown author (marked as 0), then in the model the author's popularity is assumed to be the value 0 and we get the equation:

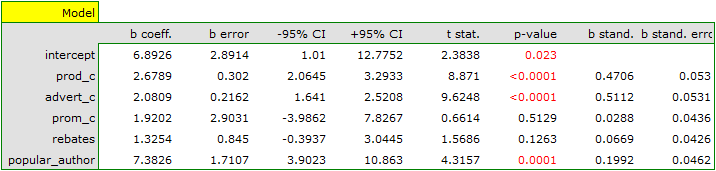

The result of t-test for each variable shows that only the production cost, advertising costs, and author's popularity have a significant influence on the profit gained. At the same time, that standardized coefficients are the greatest for those variables.

Additionally, the model is very well-fitting, which is confirmed by: the small standard error of estimation  , the high value of the multiple determination coefficient

, the high value of the multiple determination coefficient  , the corrected multiple determination coefficient

, the corrected multiple determination coefficient  , and the result of the F-test of variance analysis: p<0.0001.

, and the result of the F-test of variance analysis: p<0.0001.

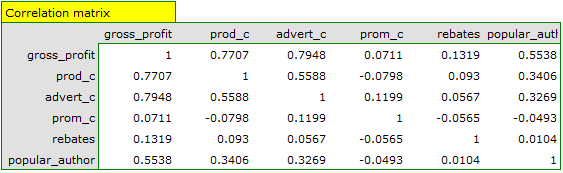

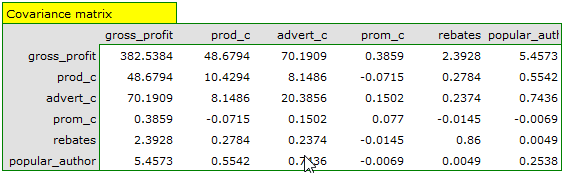

On the basis of the interpretation of the results obtained so far we can assume that a part of the variables does not have a significant effect on the profit and can be redundant. For the model to be well formulated the interval independent variables ought to be strongly correlated with the dependent variable and be relatively weakly correlated with one another. That can be checked by computing the correlation matrix and the covariance matrix:

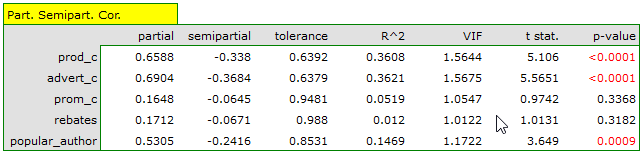

The most coherent information which allows finding those variables in the model which are redundant is given by the parial and semipartial correlation analysis as well as redundancy analysis:

The values of coefficients of partial and semipartial correlation indicate that the smallest contribution into the constructed model is that of direct promotion costs and the sum of discounts made. However, those variables are the least correlated with model residuals, which is indicated by the low value and the high tolerance value. All in all, from the statistical point of view, models without those variables would not be worse than the current model (see the result of t-test for model comparison). The decision about whether or not to leave that model or to construct a new one without the direct promotion costs and the sum of discounts made, belongs to the researcher. We will leave the current model.

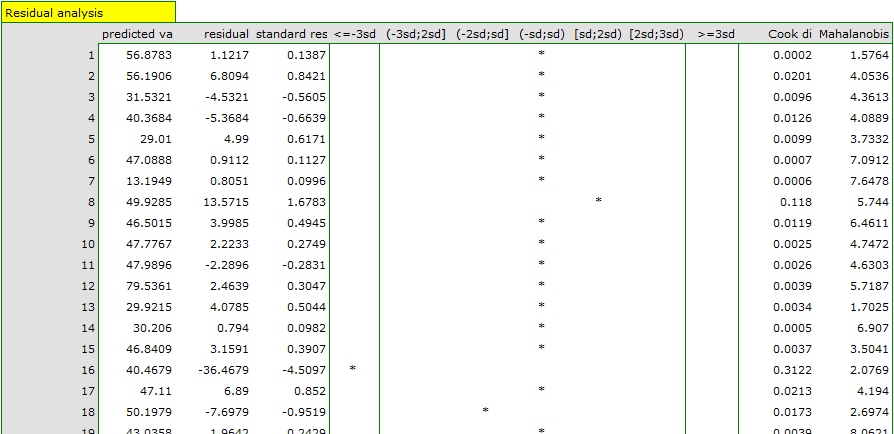

Finally, we will analyze the residuals. A part of that analysis is presented below:

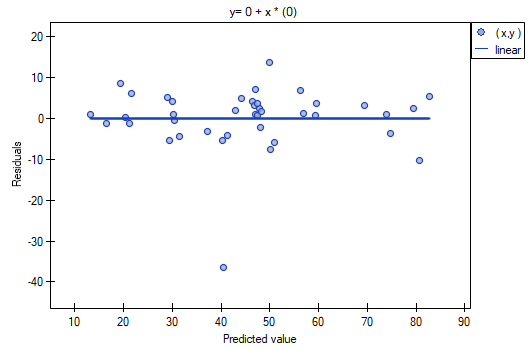

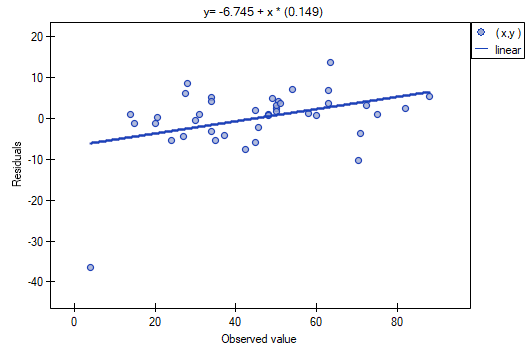

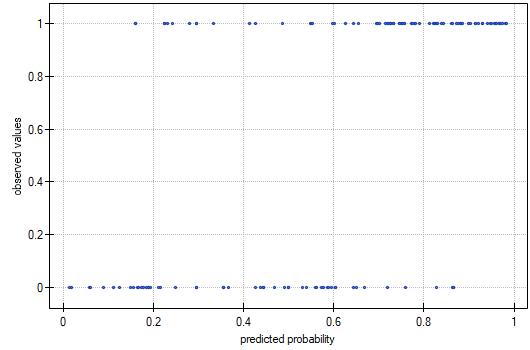

It is noticeable that one of the model residuals is an outlier – it deviates by more than 3 standard deviations from the mean value. It is observation number 16. The observation can be easily found by drawing a chart of residuals with respect to observed or expected values of the variable .

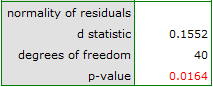

That outlier undermines the assumption concerning homoscedasticity. The assumption of homoscedasticity would be confirmed (that is, residuals variance presented on the axis would be similar when we move along the axis  ), if we rejected that point. Additionally, the distribution of residuals deviates slightly from normal distribution (the value

), if we rejected that point. Additionally, the distribution of residuals deviates slightly from normal distribution (the value  of Liliefors test is p=0.0164):

of Liliefors test is p=0.0164):

When we take a closer look of the outlier (position 16 in the data for the task) we see that the book is the only one for which the costs are higher than gross profit (gross profit=4 thousand dollars, the sum of costs = (8+6+0.33+1.6) = 15.93 thousand dollars).

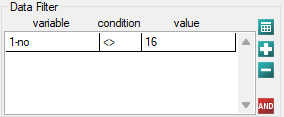

The obtained model can be corrected by removing the outlier. For that purpose, another analysis has to be conducted, with a filter switched on which will exclude the outlier.

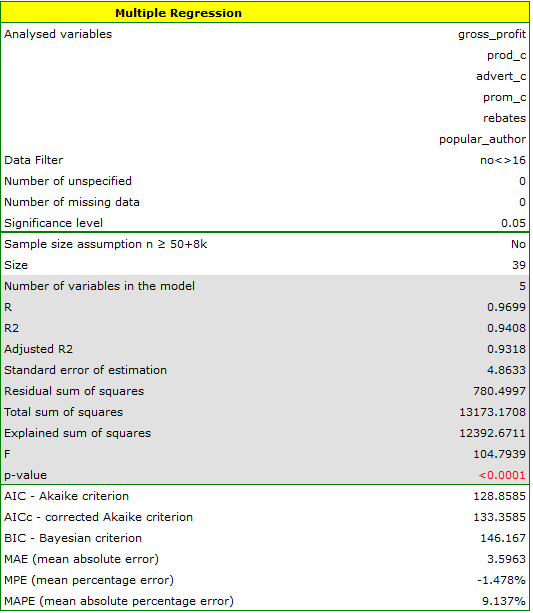

As a result, we receive a model which is very similar to the previous one but is encumbered with a smaller error and is more adequate:

![\begin{displaymath}

profit_{gross}=6.89+2.68(c_{prod})+2.08(c_{adv})+1.92(c_{prom})+1.33(discounts)+7.38(popul_{author})+[4.86]

\end{displaymath}](/lib/exe/fetch.php?media=wiki:latex:/imge53ed59a726b1c5c3e27b9d05c9cccad.png "LaTeX")

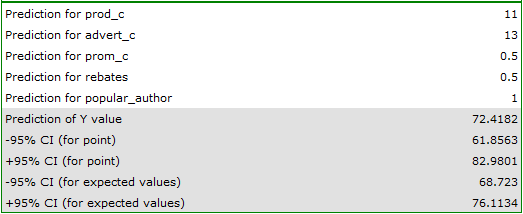

The final version of the model will be used for prediction. On the basis of the predicted costs amounting to:

production cost thousand dollars,\\advertising costs thousand dollars,\\direct promotion costs thousand dollars,\\the sum of discounts made thousand dollars,\\and the fact that the author is known (the author's popularity  ) we calculate the predicted gross profit together with the confidence interval:

) we calculate the predicted gross profit together with the confidence interval:

The predicted profit is 72 thousand dollars.

Finally, it should still be noted that this is only a preliminary model. In a proper study more data would have to be collected. The number of variables in the model is too small in relation to the number of books evaluated, i.e. n<50+8k.

Model-based prediction and test set validation

Validation

Validation of a model is a check of its quality. It is first performed on the data on which the model was built (the so-called training data set), that is, it is returned in a report describing the resulting model. In order to be able to judge with greater certainty how suitable the model is for forecasting new data, an important part of the validation is to become a model to data that were not used in the model estimation. If the summary based on the treining data is satisfactory, i.e., the determined errors coefficients and information criteria are at a satisfactory level, and the summary based on the new data (the so-called test data set) is equally favorable, then with high probability it can be concluded that such a model is suitable for prediction. The testing data should come from the same population from which the training data were selected. It is often the case that before building a model we collect data, and then randomly divide it into a training set, i.e. the data that will be used to build the model, and a test set, i.e. the data that will be used for additional validation of the model.

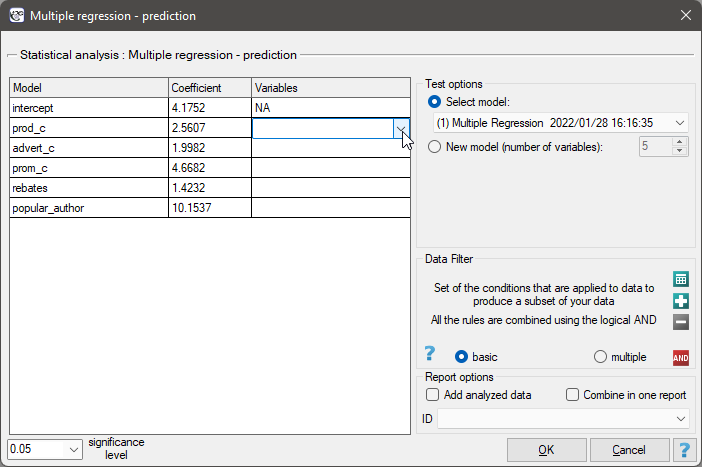

The settings window with the validation can be opened in Advanced statistics→Multivariate models→Multiple regression - prediction/validation.

To perform validation, it is necessary to indicate the model on the basis of which we want to perform the validation. Validation can be done on the basis of:

- multivariate regression model built in PQStat - simply select a model from the models assigned to the sheet, and the number of variables and model coefficients will be set automatically; the test set should be in the same sheet as the training set;

- model not built in PQStat but obtained from another source (e.g., described in a scientific paper we have read) - in the analysis window, enter the number of variables and enter the coefficients for each of them.

In the analysis window, indicate those new variables that should be used for validation.

Prediction

Most often, the final step in regression analysis is to use the built and previously validated model for prediction.

- Prediction for a single object can be performed along with the construction of the model, that is, in the analysis window

Advanced statistics→Multivariate models→Multiple regression, - Prediction for a larger group of new data is done through the menu

Advanced statistics→Multivariate models→Multiple regression - prediction/validation.

To make a prediction, it is necessary to indicate the model on the basis of which we want to make the prediction. Prediction can be made on the basis of:

- multivariate regression model built in PQStat -simply select a model from the models assigned to the sheet, and the number of variables and model coefficients will be set automatically; the test set should be in the same sheet as the training set;

- model not built in PQStat but obtained from another source (e.g., described in a scientific paper we read) - in the analysis window, the number of variables and the coefficients on each of them should be entered.

In the analysis window, indicate those new variables that should be used for prediction. The estimated value is calculated with some error. Therefore, in addition, for the value predicted by the model, limits are set due to the error:

- confidence intervals are set for the expected value,

- For a single point, prediction intervals are determined.

Example continued (publisher.pqs file)

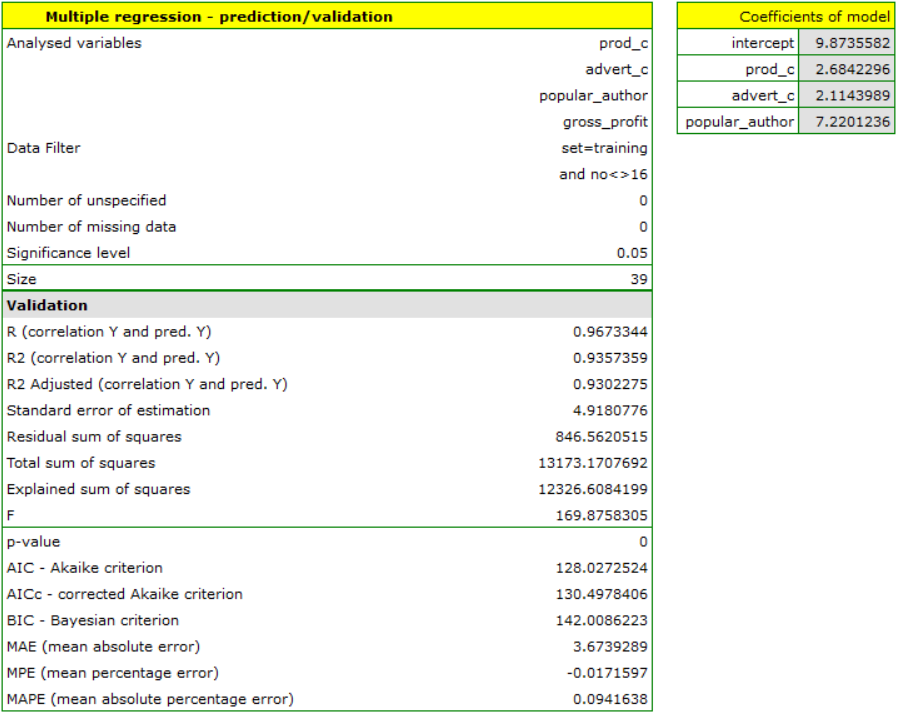

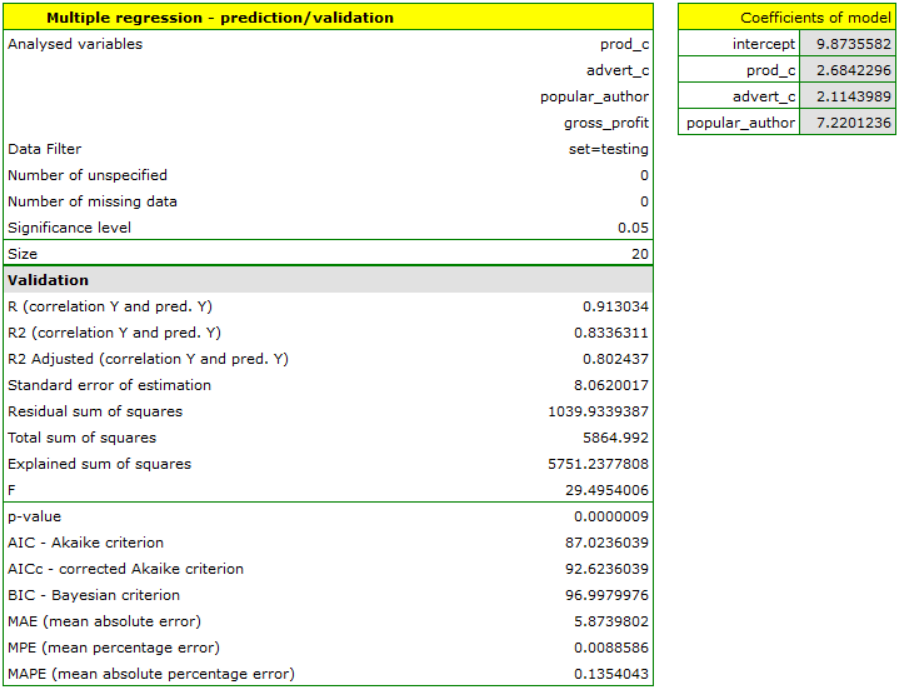

To predict gross profit from book sales, the publisher built a regression model based on a training set stripped of item 16 (that is, 39 books). The model included: production costs, advertising costs and author popularity (1=popular author, 0=not). We will build the model once again based on the learning set and then, to make sure the model will work properly, we will validate it on a test data set. If the model passes this test, we will apply it to predictions for book items. To use the right collections we set a data filter each time.

For the training set, the values describing the quality of the model's fit are very high: adjusted = 0.93 and the average forecast error (MAE) is 3.7 thousand dollars.

For the test set, the values describing the quality of the model fit are slightly lower than for the learning set: Adjusted = 0.80 and the mean error of prediction (MAE) is 5.9 thousand dollars. Since the validation result on the test set is almost as good as on the training set, we will use the model for prediction. To do this, we will use the data of three new book items added to the end of the set. We'll select Prediction, set filter on the new dataset and use our model to predict the gross profit for these books.

It turns out that the highest gross profit (between 64 and 85 thousands of dollars) is projected for the first, most advertised and most expensive book published by a popular author.

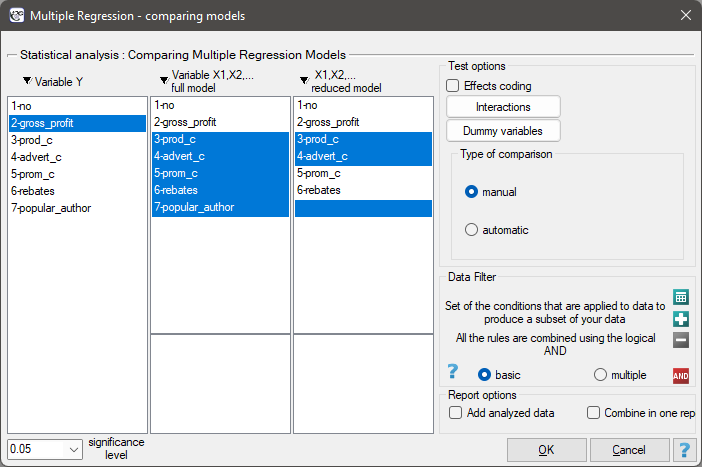

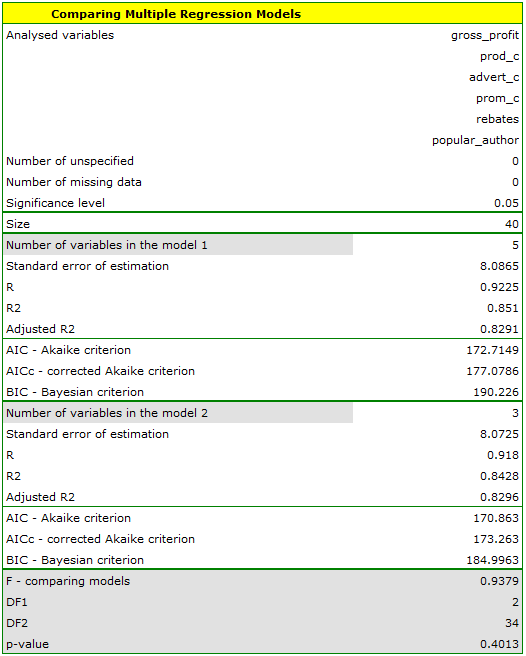

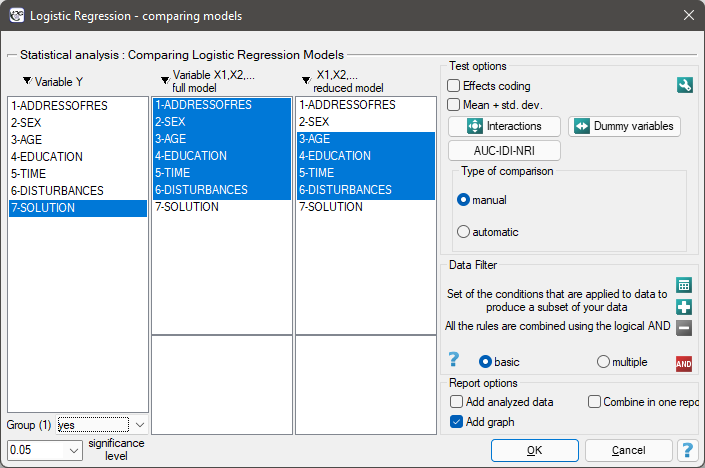

Comparison of multiple linear regression models

The window with settings for model comparison is accessed via the menu Advenced statistics→Multidimensional models→Multiple regression – model comparison

The multiple linear regression offers the possibility of simultaneous analysis of many independent variables. There appears, then, the problem of choosing the optimum model. Too large a model involves a plethora of information in which the important ones may get lost. Too small a model involves the risk of omitting those features which could describe the studied phenomenon in a reliable manner. Because it is not the number of variables in the model but their quality that determines the quality of the model. To make a proper selection of independent variables it is necessary to have knowledge and experience connected with the studied phenomenon. One has to remember to put into the model variables strongly correlated with the dependent variable and weakly correlated with one another.

There is no single, simple statistical rule which would decide about the number of variables necessary in the model. The measures of model adequacy most frequently used in a comparison are:  – the corrected value of multiple determination coefficient (the higher the value the more adequate the model), – the standard error of estimation (the lower the value the more adequate the model) or or information criteria AIC, AICc, BIC (the lower the value, the better the model). For that purpose, the F-test based on the multiple determination coefficient can also be used. The test is used to verify the hypothesis that the adequacy of both compared models is equally good.

– the corrected value of multiple determination coefficient (the higher the value the more adequate the model), – the standard error of estimation (the lower the value the more adequate the model) or or information criteria AIC, AICc, BIC (the lower the value, the better the model). For that purpose, the F-test based on the multiple determination coefficient can also be used. The test is used to verify the hypothesis that the adequacy of both compared models is equally good.

Hypotheses:

where: